Aqua Bounty - Case Solution

As an emerging biotechnology company, Aqua Bounty is continuing to expand with two major products in the pipeline. One of these two products is the AquAdvantage, a genetically modified strain of fish to enhance the growth rates significantly. This case study seeks to find out the value of the AquAdvantage opportunity.

Case Questions Answered

- What was the value of the AquAdvantage opportunity of Aqua Bounty?

This case solution includes an Excel file with calculations that will be available after purchase.

This case solution includes an Excel file with calculations.

Overview – Aqua Bounty

As an emerging biotechnology company, Aqua Bounty is continuing to expand with two major products in the pipeline.

The first of these, a shrimp therapeutics product, Shrimp IMS, enhances shrimp’s immune system for commercial farming. Aqua Bounty plans to launch the product within 12 months with a large potential market and high hopes.

The second product, AquAdvantage is a genetically modified strain of fish to enhance the growth rates significantly. AquAdvantage is another product with strong market potential for AquaBounty. However, approval from the FDA and other regulatory barriers stand in the way of commercialization.

Furthermore, public perceptions of the product are a risk area for Aqua Bounty. As a result, the commercial success of the product is unknown. To overcome the final development period, before product revenues can be realized, funding through an initial public offering will be required.

The upside of these products should provide great interest from the market, but numerous conditions must proceed in favor of Aqua bounty for the full value to be realized.

Challenges in valuing the company

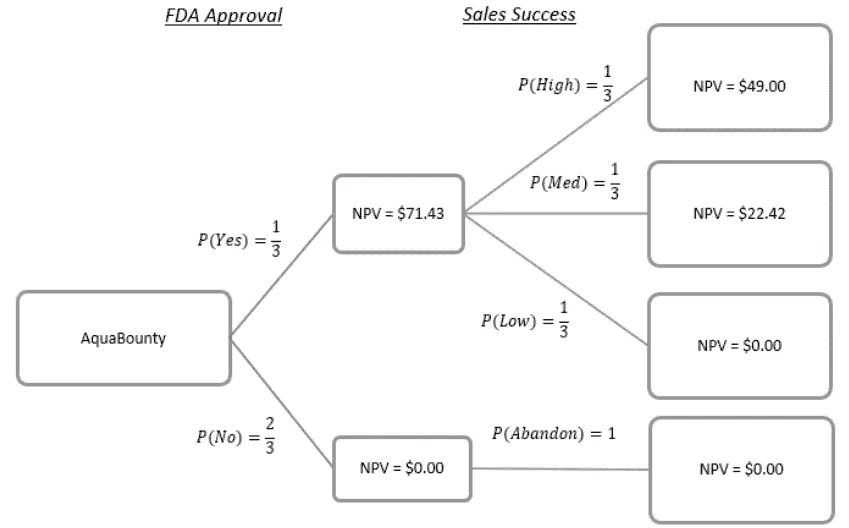

There are two major uncertainties about the company’s future, namely FDA approval and customer acceptance.

Firstly, Aqua Bounty is uncertain whether the FDA will approve the sales of genetically modified products and when it will happen.

Secondly, once the approval is granted, it is uncertain whether the customers will be receptive to genetically modified fish with the concerns of safety and environmental issues.

Valuation result (DCF)

Once the FDA approval is granted, the AquAdvantage division is sitting on a valuation of $71.43. This is discounted from the three scenarios of revenue growth as a result of various

customers’ acceptance.

There are equal probabilities that the division will achieve high, base, and low revenues depending on the market and the customers’ reactions to the genetically modified fish.

With the provision of the baseline projection, the revenue under the pessimistic scenario will be 75% lower than that of the baseline, and revenue under the optimistic scenario will be 75% higher than that of the baseline.

If all goes well, a value of $49m is…

- Full written analysis

- All case questions answered

- Excel spreadsheet included

- Instant delivery to your email

By clicking “Get Instant Access”, you agree to our Terms of Use, Arbitration and Class Action Waiver Agreement and Privacy Policy